Alphabet (GOOG)

Alphabet (GOOG). Looking into the king of search, the pioneer of work culture, and the research company that has a side gig of advertising.

It’s a daunting task to look at an extremely large (and equally complex by result) company as Alphabet (GOOG). It’s a product that touches many aspects of everyone’s life.

I use Youtube to learn and use it as a proxy for TV, I use Gmail, Googling became a verb for searching for answers to questions, chrome was a default browser for a while, I used to use an android phone etc…. We see it in homes with Nest, some use it to pay with Google Pay. The list goes on and on.

At the highest level, it’s an advertising company. A massive digital billboard that shows products of other companies. A company that serves its clients (advertisers) and users (you and me) through its various ‘monetarily free’ services (there aren’t any ‘truly’ free lunches right?).

IPO History

GOOG was founded in 1998. I think… until 2002, I was using Yahoo and MSN as may main search engines. GOOG may have come up from time to time but it was never a default until much later.

It IPO’d in 2004 with an ‘auction IPO’, which was untraditional at the time and I think it still is uncommon since it leaves the judgment of the share price up to the investors to set prices and bankers servicing the IPO would love a higher priced IPO for their commissions. I also imagine most VC funds that back IPOs want the big pumped up share prices vs. letting the market set the value.

I mean, it makes sense from their first letter: “An auction is an unusual process for an IPO in the United States. Our experience with auction-based advertising systems has been helpful in the auction design process for the IPO. As in the stock market, if people bid for more shares than are available and bid at high prices, the IPO price will be higher. Of course, the IPO price will be lower if there are not enough bidders or if people bid lower prices. This is a simplification, but it captures the basic issues.”

Regardless, it IPO’d in 2004 at $23B market cap, which was at ~10x P/S. Food for thought there. It’s 6x P/S as of late June 2020. Despite the decline in P/S multiple, you still made a CAGR of ~19% over the 16 years.

The actual company history is something that many of us (once again) have superficial knowledge on. The classic two PhDs building a business out of a garage (literally).

Unconventional

“Google is not a conventional company”. This is how the 2004 shareholder letter started as Larry Page & Sergey Brin (Co-Founders of GOOG) wrote out the Owners Manual for GOOG. Much of the 2004 letter hints at the influence that Warren Buffett had on the business and how they look at investing in the long-term growth of the company.

Their auction-IPO was unconventional but so was much of the culture they created. If I think about companies that created cultures… GOOG would probably be the one responsible for all the “perks” tech companies boast today. But I imagine a company offering catered meals, open-concept offices, nap pods, fitness centers etc… was not seen positively in the early 2000s.

Looking after employees with great benefits and perks might seem table stakes for ‘tech’ companies now but GOOG led the way.

In one way, GOOG may have known early on that they were an advertising/media company given their, once again, unconventional use of a dual class structure per the 2004 letter: “While this structure is unusual for technology companies, similar structures are common in the media business and has had a profound importance there. The New York Times Company, The Washington Post Company and Dow Jones, the publisher of The Wall Street Journal, all have similar dual class ownership structures. Media observers have pointed out that dual class ownership has allowed these companies to concentrate on their core, long term interest in serious news coverage, despite fluctuations in quarterly results. Berkshire Hathaway has implemented a dual class structure for similar reasons. From the point of view of long term success in advancing a company’s core values, we believe this structure has clearly been an advantage.”

Jumping back on culture, I also think GOOG is the company that made it “acceptable” to call its own people with their own name (Googlers). Why not? GOOG is a nation (albeit better run and more powerful than what we call “countries” in this day and age). So yeah, I think they may have been crucial contributors in changing the mindset around what an organization’s responsibilities are to its people.

GOOG & I & Money

Okay. It’s unconventional.

It interacts with various facets of my life via GOOG Maps, Photos, Lens, Play, Youtube, Android, Chrome, Gmail, Gsuite (I’m writing this on Google Docs and numbers are on Google Sheets). Oh and Google Cloud.

Those are the main products we know.

Then are the ‘moonshot’ companies like Nest (your home), Calico (tackling aging?), Capital G (financing… like a bank), GV (a venture capital fund), Wing (drone deliveries), Waymo (self-driving cars), Fiber (internet for the world), Verily Life Science (fighting diseases and health problems), DeepMind (AI) and all kinds of things to AI detection of cancer (lung + breast) and everything else….

It does a lot. I mean, it’s one of the largest (fighting in the top 3 positions) by market cap.

But despite all the kinds of things it does for you, me and the world… it’s an advertising company. Weird, because I associate advertising with ‘slimy, shitty, wrong’ yet GOOG has created so much surplus for my life.

Maybe it’s because of GOOG’s evolving mission?

2004 was "Serving our end users is at the heart of what we do and remains our number one priority.”

2017’s letter said: "While I am optimistic about the potential to bring technology to bear on the greatest problems in the world, we are on a path that we must tread with deep responsibility, care, and humility. That is Alphabet’s goal."

Combined with 2018’s "we’ve evolved from a company that helps people find answers to a company that helps you get things done.”

They also used to say “Don’t be evil” but they no longer advertise that as part of the company value… maybe they realized the line of good and bad is so blurry it gets harder the more complex a system becomes?

But okay, so let’s talk $$$.

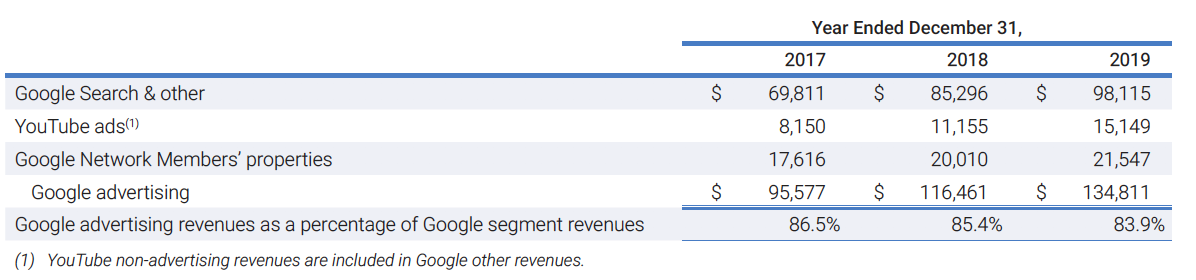

~80%+ of revenues have come from advertising. GOOG Network Members include ad spends on properties like AdMob, AdSense, Google Ad Manager. Youtube is simple. And ‘Search & other’ includes every ad we see on a GOOG property like on chrome, search, Gmail, Maps etc…

Cloud (GCP) is small but its rapid growth is a contributing factor to the mix of revenue slowing declining from advertising over the years. As management notes: "Google Cloud is one of the largest areas of investment for Google, and it continues to be a big bet for us. Helping businesses realize their missions is a big part of how we realize ours, and we are committed to being a strong technology partner for the long term."

GOOG other is the Youtube subscription, licenses from the Play store, hardware sales (Pixel, Nest, Home, Chromebooks) and other ‘small things’. The Other Bets are all the other moonshots I listed from before that makes it seem like GOOG’s about to make my life even easier and better…. Like rescuing humanity from all the inconveniences of the world.

Customers.

Simply everyone. For advertising (~84% of sales) its various enterprises. GOOG doesn’t share concentration. But I found some data in 2011 where GOOG’s largest ad spender (Lowe’s) made up 0.1% of total sales. The data is quite out of date. In 2019, Expedia + Booking combined to spend ~$11B on advertising at GOOG. Making up about ~7% of ad revenue between the two. With the COVID hit on travel in 2020, this will take a hit for sure.

I would imagine a 3-4% revenue concentration to be the highest. Using Facebook (FB) as a proxy, Home Depot is est. to be their largest ad spender at $150M in 2019 and that makes up ~0.2% of FB’s ad revenue.

So, all kinds of companies advertise on GOOG and they will take a bit of a hit from the travel decline. As far as GCP goes, it includes enterprises like Home Depot, PayPal, Target, HSBC, Bloomberg etc.. Once again, no idea on the concentration but I imagine it’s small.

Advertising is a discretionary spend by customers and there really are no long-term contracts. Naturally, this means there can be a cyclicality to it as economic activity can impact advertising spends. A la COVID. But, some ad spend will be hit less than others…. And that’s where the reach + cost of the platform will factor into the ROI equation.

Though companies might dedicate big budgets to digital ads, the cost per deployment is low. It’s not a big ticket commitment like a billboard or TV ad. From conversations I’ve had with friends who are in marketing, ~20-30% of ad dollars go to GOOG and 40-50% to FB. Now, it’s all case by case and different industries have different platforms they focus on. But, GOOG will get a good chunk of the spend. It’s also usually a comparison of ROIs on GOOG vs. FB and they tend to have better ROIs than other platforms just by the sheer amount of data they have and how advertisers can play around with the products. It’s an extension of the argument I made deeper on when I looked at Pinterest.

Market + Users.

GOOG is still the no.1 platform for global digital ad spend. It commands a ~31% market share and FB at ~20%. Generally, the global ad market seems to be concentrated to GOOG, FB and AMZN.

https://www.emarketer.com/content/global-digital-ad-spending-2019

Then you consider taking a look at search and other than China, GOOG is the big dog. What’s surprising is to see GOOG is now ahead of Yandex in Russia. I did not think that was possible. But globally, they have 90+%.

https://alphametic.com/global-search-engine-market-share

I think another big market folks look at for GOOG is in cloud infrastructure and they are in 3rd place, recently surpassing IBM I think.

But my greatest fascination is with Youtube. I’m not sure how you’d compare it… because it’s a social platform that is in the competition for attention. So one can look at it among a group social products as below:

But it’s specifically video streaming. If I consider ‘live streaming’, it can arguably be competing with Twitch and Instagram but they are both unique in their use cases as well. I mean, Twitch blows Youtube out when it comes to its niche of gaming:

Overall, the point is that GOOG is a major player in the markets it plays in. That was probably obvious even before doing any research in the company. But, it’s nice to put everything into perspective when it comes to ad spend, how big search is, who runs the cloud and where Youtube fits in with FB’s engines.

Costs & Margins

I particularly like looking at gross margins. In most cases, since I like learning about companies that are constantly reinvesting to grow, anything below gross profit tends to look ugly. But gross margins give me an indication of the basic economics. If I sell a widget for $10, and it costs $4 to make… then i get to keep $6. Much of the costs of producing the goods (COGS), including customer support in cases of services, are included in the COGS so that’s where gross margin (GM) comes in.

As expected, GOOG has a rather high GM exceeding 50%. It’s historically been in the mid 60% 10 years ago (2010/2011) but it’s come down in recent years to the mid-50%.

What is TAC? Traffic Acquisition Cost. I had no idea GOOG paid to have traffic come to them. It’s kind of meta…. Marketing teams of large companies will pay google to acquire customers (many showing it as CAC), but GOOG pays other companies to acquire users onto their site. The users being the product they sell to the large companies for advertising.

TACs are basically fees GOOG pays partners/services to direct traffic to the GOOG search engines/platforms. A simple example is GOOG paying Apple (AAPL) billions (I heard ~$10bn). A part of that deal includes making GOOG the default search engineer for Safari. Same for all the other browsers out there. As GOOG notes: distribution partners include browser providers, mobile carriers, original equipment manufacturers, and software developers"

The TAC % of Ad revenue is one proxy for looking at GM for the ad business. Adding to the image above, the 2018 and 2019 TAC % of ad sales was ~22% for each year. A steady state (if I dare to imagine) may be in the low-20s…. Or maybe I should say that is the lower bound. It could always get higher. I don’t know if GOOG will cancel paying TAC to its partners… though they are the dominant provider and they may have power over their suppliers… I wonder if it’s as simple as that. Regulators may not want to hear complaints regarding the monopoly of search not paying its partners anymore.

So, this makes the ad business look like it’s recent GMs should be in the ~70%s…. Is the other part of the business not pulling its weight? A yes and no.

As GOOG points out in regards to the ‘other cost of revenues’ it includes: "Content acquisition costs primarily related to payments to content providers from whom we license video and other content for distribution on YouTube advertising and subscription services and Google Play (we pay fees to these content providers based on revenues generated or a flat fee)" + "Expenses associated with our data centers and other operations (including bandwidth, compensation expenses (including stock based compensation (SBC)), depreciation, energy, and other equipment costs);"

It’s hard to say what parts of the other costs would have contributed to the Youtube ad sales or the entire GOOG ecosystem given in includes compensation for the people who probably manage all the customer support components.

Not all Ads are equal.

Turns out, Youtube ads monetize at a lower rate than search ads. A possible tailwind to GM as Youtube grows and search declines? I think this the more likely scenario given my biased favouritism for Youtube.

Also, mobile ads have lower gross margins than desktop ads (though FB commands a 80%+ GM despite a mobile dominant platform… I wonder how they make this possible). Could this mean that GOOG’s mobile ads are not as valuable as FBs? Possibly. Could this lead to further GM compression with the growth of mobile? Maybe.

GOOG has been vocal about expanding ex-US and the geographic revenue mix shows increases there (not material though). At the moment, international markets also have lower margins than the domestic US market. So, further margin compression?

Maybe I should be expecting margins to continuously compress over time while the raw volume increases.

Reinvestment.

Given GOOG’s focus on innovation, R&D is a major expense area for the business. They also have functions of growth CAPEX to consider as well: “....trend to continue in the long term as we invest heavily in land and buildings for data centers and offices, and information technology infrastructure, which includes servers and network equipment.”

Though, I do not know how much is actually spent on the data centers… But, once again, let’s take a shot at looking at GOOG’s return on investments to get an idea of whether it’s “high” or not.

A criticism I’ve heard relating to GOOG is that they are not great at deploying capital.

Cash makes up nearly 50% of their total assets and some are critical of that. Their debt is negligible so it’s practically $110B of net cash on their BS. Investors give Japanese and Korean companies a lot of flack for having high cash on their BS. Less do for US tech companies (who knows why…..though I imagine it’s more psychological). But at times of crisis, cash is king and GOOG’s got plenty of it!

So, when they deploy their cash what return do they get? I use quickfs.net for quick financials and the last 6 year average I get from there is a ROIC of 16.3%. Over that same period, share price grew at a CAGR of ~16%. Quite in line with the saying that over time, the business will return the rate it returns investment on capital.

But I like to look at ROCE differently by capitalizing the reinvestment in human capital. Over time, this gives me a ROCE of ~32% (6 year average), with recent years closer to ~25%. Compared to the traditional approach, this looks higher and yeah it may be that I’m wrong. But I was curious so I looked at the share price movements for my past research on WIX, SPOT, and TEAM and they are relatively close to my ROCE. But, I’m looking at 2 years vs. 6 years for those younger companies… so maybe my calculation is more applicable for a faster-growing/younger company that has to plow more into human capital? I’m not sure. I could also be flat out wrong in my methodology as well. Even if it feels like it makes sense to me.

Regardless, I get a ROCE of 25-30% for GOOG. Touching briefly on valuation, at the current EV of ~$850B, I get a yield of ~4% on owner’s earnings. Hmm… what about growth? You’d think it’s got plenty of growth potential given the yield provided by the market.

At the base, advertising spend tends to grow in-line with GDP…. making me think that the organic growth rate in ad spends would be ~4%. I don’t imagine GOOG to lose its dominance drastically. It may not win all new opportunities but I’m sure it will defend its position well.

Now, gross profit has grown at an avg rate of ~17% over the last 10 years. Will it continue? Who knows…. They could grow at 17% for another 10 years. They also might not. But I could see returns ranging between 8% to 30% over the long term. I might be giving it a pretty narrow band…. But seems reasonable.

Management

Page and Brin control GOOG with 52% of the votes.

Though, they aren’t as involved in the day to day operations as GOOG anymore. Page was the CEO of Alphabet and Brin its President but both stepped down to remain on the BoD as “Co-Founder & Director” in late 2019, making Sundar Pichai the CEO of both Google & Alphabet.

It’s not something I like to see. I prefer to see the founders/owners to be involved in the business. I don’t know how involved they were before and I don’t know how this will change their relationship with the business in the future. Something I’m not privy to unfortunately.

But what I like seeing is consistency in the Co-Founder’s ownership of the business. They have sold off some of their Class B shares since the 2012 YE Proxy statement below but it hasn’t been material. It’s also a positive signal to see John Doerr and Eric Schmidt maintain similar levels of ownership as before.

They’ve also not abused their controlling position in the business with extravagant salaries either. Whether it was in 2012 when they were running the business with Schmidt:

Or in 2019 with Pichai, they sold portions of their ownership to live. It’s just a class move.

Compensation metrics have also evolved. The Co-founders opted to cancel annual bonuses and only have salary and biennial equity compensation for execs to focus on long-term value creation.

This is a constant theme that I noticed in the many letters to shareholders. A focus on the long-term. The Co-founders continuously reference how GOOG is not a conventional company and they will continue to take bets that will not result in short term gains.

Another interesting element to this long-term mindset is how they’ve periodically referred to GOOG as a human. In the early 2010s, they referred to GOOG as a teenager and as they departed from their roles in 2019 they said: “Today, in 2019, if the company was a person, it would be a young adult of 21 and it would be time to leave the roost. While it has been a tremendous privilege to be deeply involved in the day-to-day management of the company for so long, we believe it’s time to assume the role of proud parents - offering advice and love, but not daily nagging!"

Regarding the depth of the current management team, Pichai has been with GOOG since 2005, Porat joined in 2015 and Drummond joined in 2002. As Drummond retires, it will be interesting to see if GOOG promotes from within. Pichai was groomed to be the CEO but that wasn’t the case for his predecessor, Schmidt. Schmidt joined GOOG from a CEO role at Novell and if I’m remembering correctly, John Doerr (BoD member since 1999 at GOOG) and Bill Campbell (The Trillion Dollar Coach) were crucial in convincing him to join GOOG as CEO. That alone is a fascinating story worth hearing from Schmidt’s many podcast interviews and the biography of Bill Campbell.

GOOG doesn’t take leadership transitions lightly and the stories of how they think about it are fascinating too.

If I had to nitpick at something… it’s the compensation method. Much of Pichai (and other exec’s) equity compensations are in GSUs that vest over 3 years and about 30% of the equity comp in PSUs (performance based stock units). Yes, the performance based amount is low.

Even the way performance is calculated is focused on TSR. Not any internal metric. I would obviously prefer to see 100% in PSUs that use some kind of ROI + growth metric… given how the company started out taking a learning from Buffett, this kind of compensation measurement is disappointing.

But, GOOG has made change to its compensation over time. It moved away from stock option to restricted stock awards in 2012. Same for only issuing long-term equity vs. annual incentives. So, maybe they will make further changes that focus on long-term value creation over time.

As far as whether compensation is outrageous or not. I don’t think it is. The Co-founders set the culture early on prudence and I don’t see financial abuse happening in the future. It is an extremely high amount that Pichai is getting.. In addition to the $100M he received in 2015… but in relative context, this is GOOG. And equity awards happen infrequently…. It’s more so that I trust this board and management team to be fair.

A quick pivot to culture.

I don’t know how much I can say on this. There are so many essays on GOOG’s culture. There are even books. Now, it’s continuously evolved but what is apparent is that they give a damn.

They had earlier programs in 2004 like: “We encourage our employees, in addition to their regular projects, to spend 20% of their time working on what they think will most benefit Google.” These gave rise to Ad Sense and GOOG News.

When Alphabet was created in 2015, the focus was to create an entrepreneurial culture to foster autonomy: "A number of our projects became companies, with more autonomy and dedicated leadership.”

They also did all kinds of unconventional perks/benefits I mentioned earlier for their employees. Then there are all the rankings of ‘best place to work’ that give GOOG a top ratings everywhere.

Talent War

Much of what I say here is anecdotal… I mean, much of the report where I chime my opinion is in way anecdotal too. But I do believe GOOG has a distinct advantage over others in regards to acquiring, developing and retaining talent. GOOG’s business succeeds as a result of the Googlers.

If it’s compensation, GOOG is not shy with paying up for top people. I’ve heard top data scientists will make a few million in compensation. Not many firms can match that.

There’s also the opportunity one has while at GOOG. When I asked a data scientist friend why he left startups to join GOOG, he said for a data scientist you want to go where all the data is. Working for a scrappy startup is boring for someone who genuinely likes to sovle problems with data (GOOG’s bread and butter). Startups/fast-growing companies are great for ambitious people. But it seems like the nation of GOOG can provide such opportunities within through the Alphabet structure as well. It does so with a mountain of data problem solvers can use to play with. Most data scientists in startups build the infrastructure and have to wait for the data to pile in and unless they have a lot… it’s not valuable.

GOOG (like many of the FAANGMA!%^*@#*) are slowly becoming the defacto ‘brand’ people seek on their resume. Whether it’s engineering or business students. Nothing told me more about talent leverage than when speaking to MBA friends from the highly rated US schools and how career presentations by management consulting firms and banks have so much panache and how students and wined and dined but when GOOG comes, they don’t do anything. This reminds me of what Dave Chappelle did in his Mark Twain award ceremony when he entered the stage smoking a cigarette and he said “This is called leverage.”

They also have a global reach with offices everywhere but as far as major cities like SF, it’s hard for companies to compete against the bankroll of GOOG.

But I’ve also had numerous friends tell me it’s kind of where you go to retire. There are plenty of folks at GOOG who are uninspired and just get paid to chill. They are not exempt from the rot of a large company. It’s just not to the level of banks. But it definitely isn’t has purpose-driven and focused as it was in the earlier days (at least that’s not the case for 100% of the employees).

There is no denying that GOOG pioneered much of the practices that have become standard in investing in people and building an amazing culture…. But this may no longer be in the forefront of the behemoth anymore. It’s better than most now, but not one the best it used to be.

Still Unique @ Tackling Big Problems.

Despite the flack GOOG gets for becoming a large, slow giant…. I think it’s in the few handful of companies that are actually doing something to make people’s lives better. Yes, it’s still an advertising business. That’s where most of their money comes from. But I think GOOG is changing the narrative of the ‘slimy advertising business’.

I just don’t know of many companies that have produced so much consumer surplus. The amount of things GOOG’s created that are free…… the problems they are even tackling in AI, health, finance, infrastructure etc… I mean, at this point, I’m fine if GOOG uses all that technology to make money. It’s still creating a net win-win for society and themselves.

Compared to AAPL that focuses on making luxury goods, Microsoft that makes life easier for companies, Facebook that finds ways I can distract myself more, I think GOOG is actually doing something to fix bigger problems…. Not just making life easier for the developed world. Now, I might be giving GOOG too much credit for the ‘altruistic?’ angle…. But I think this makes the company quite unique. And they can make all this happen with a VC fund and a bank of their own.

Come to think of it…

I realize as I get ready to conclude on my initial learnings on GOOG that I have not mentioned the word ‘moat’ or ‘competitive advantage’ once. It did leave my mind. Maybe it was so obvious they had some kind of advantage that I didn’t think about mentioning it.

They have a resilient business. I think they also have a resilient culture that will make them an adaptable organization for the future. It’s a company founded by two researchers and I think that mindset has never left the company.

It’s known to be an engineer-first culture but I think it’s a research-based culture. It’s not about pumping out products fast. It’s a company that seems to be hell-bent on making the world better. I think they will continue to do well over time. Not saying they’ll be dominant in advertising forever. Everyone is coming after them. The government, the companies, the entrepreneurs etc… It’s a tough position to be in.

Disclaimer - I’m writing this for myself. For my past, present and future self. Much of what I write is my opinion. If it somehow ignites agreement in you then great, I’d love to hear about it. If it sparks disagreement in you, don’t reach out because I don’t care for it. There always are obvious exceptions and the flawed person in me hasn’t considered them all.